Covariance Matrix

Covariance Matrix is a type of matrix used to describe the Covariance values between two items in a random vector.

Resources

- https://www.geeksforgeeks.org/covariance-matrix/

- Practice implementing this: https://www.deep-ml.com/problems/10

General formula

- Since

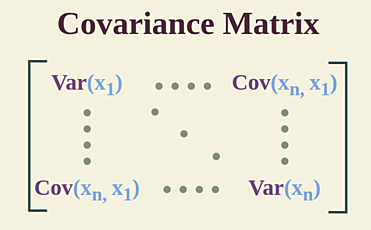

We use a covariance matrix to denote covariances of a multivariate normal distribution, and it looks like this:

\Sigma = \begin{bmatrix} \sigma_1^2 & \sigma_{12} & \cdots & \sigma_{1n} \\ \sigma_{21} & \sigma_2^2 & \cdots & \sigma_{2n} \\ \vdots & \vdots & \ddots & \vdots \\ \sigma_{n1} & \sigma_{n2} & \cdots & \sigma_n^2 \end{bmatrix}$$ The diagonal contains the variance for each variable, and the off-diagonal elements contain the covariance between the $i^{th}$ and $j^{th}$ variables. So $\sigma_3^2$ is the variance of the third variable, and $\sigma_{13}$ is the covariance between the first and third variables. The covariance matrix is a symmetric matrix. ### Related [[notes/CMA-ES|CMA-ES]]